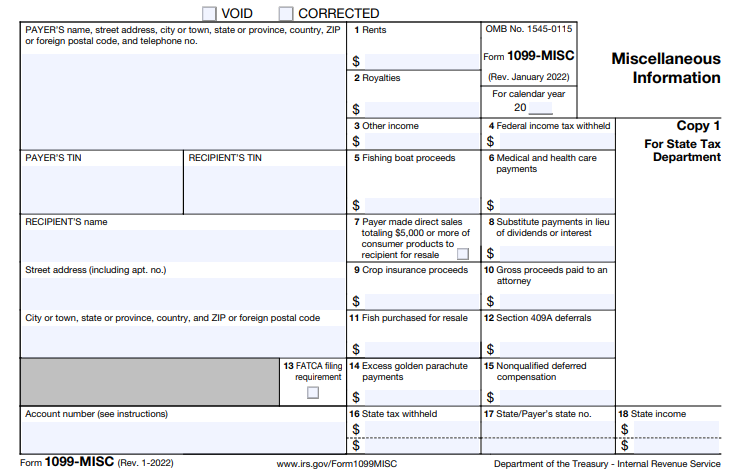

2: Royalties – intangible property, which include patents, copyrights, trade names, payments from oil, gas and mineral properties, and payments to authors or artists for use of their works.

3: Other income – any other payments made over $600 that don’t correspond to another box on the 1099-MISC as well as prizes or awards that are not for services performed.

4: Federal income tax withheld

5: Fishing boat proceeds – any amount paid out from a sale of a catch

6: Medical and health care payments – if you pay individuals for healthcare-related services, like drug screening, you would record those payments here. (This does not apply to payments made for healthcare premiums.

7: Payor – you just need to check the box if you made direct sales of $5,000 or more to a recipient for resale, and then provide a separate report of those direct sales transactions.

8: Substitute payments in lieu of interest – this typically applies when there is a loan of a customer’s securities and interest is accrued as a result.

9: Crop insurance proceeds

10: Gross proceeds paid to an attorney – there’s more fine print related to this one, so if you have any legal situations you’ll want to speak with your CPA.

11: Fish purchased for resale

12: Section 409A deferrals – first, check Notice 2008-115 because you may not have to fill out this section.

13: Excess golden parachute payments – compensation payments made to a disqualified person relating to a change in control of a corporation.

14: Nonqualified deferred compensation