Ways We Look Out for Your Business From operating accounts...

Read More

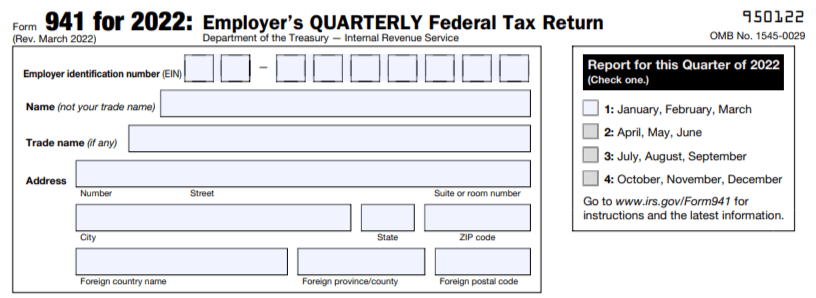

Employers are required to withhold, Medicare tax, and Social Security tax from employees. Employers report the total withheld payroll tax during the quarter in Form 941. On Form 941, you must report things like wages paid to employees, federal income taxes withheld, and FICA tax (both employee and employer portions). The IRS compares the amounts on your four quarterly forms to your annual Form W-3.

• Basic business information, such as name, address, and Employer Identification Number (EIN)

• Number of employees you compensated during the quarter

• Total wages you paid to employees in the quarter

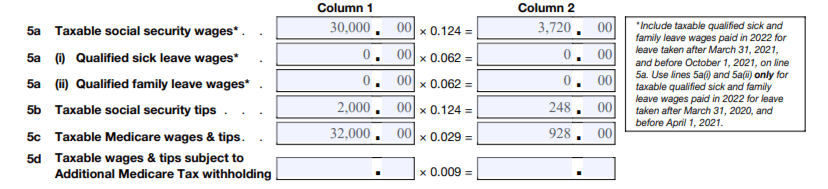

• Taxable Social Security and Medicare wages for the quarter

•Total federal income, Social Security, and Medicare taxes withheld from employees’ wages during the quarter

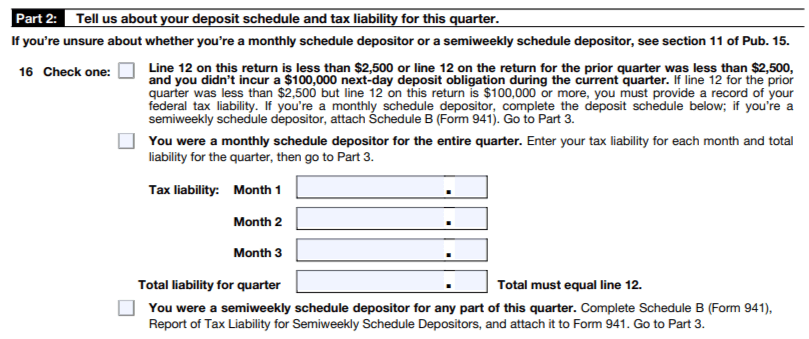

• Employment tax deposits you’ve already made for the quarter

• Information about paid sick or family leave wages, if applicable

• COBRA premium assistance credit information, if applicable

• Wages paid to employees

• Federal income taxes withheld

• FICA tax (employee and employer contributions)

• Reported tips

• Additional taxes withheld

In addition to the above information, you need to include any adjustments to Social Security and Medicare taxes, sick pay, tips, and group-term life insurance.

Submit Form 941 even if you do not have any 941 taxes to report.

• January – March (Quarter 1): April 30th

• April – June (Quarter 2): July 31st

• July – September (Quarter 3): October 31st

• October – December (Quarter 4): January 31st

If one of the due dates winds up falling on a weekend or legal holiday, the form is due the following business day.

If you miss the due date, you might be subject to a penalty. You might also face penalties if you make late tax payments.

For each month (or partial month) late for filing, the IRS imposes a 5% penalty. The maximum penalty is 25%.

If your payment is one to five days late, the IRS will also tack on a penalty of 2% of the unpaid tax. Deposits that are six to 15 days late are subject to a 5% penalty. If your payment is more than 16 days late, the IRS charges a 10% penalty. In addition to penalties, the IRS also charges interest on unpaid balances.

Keep in mind that the IRS might waive certain penalties if you have reasonable cause for filing late.

You can avoid Form 941 penalties by filing Form 941 on time, paying taxes when they’re due, and accurately reporting your tax liability.

Like with anything in business, there is a potential for error when it comes to filling out Form 941. If you make an error on Form 941, don’t panic. Instead, use Form 941-X to make corrections. You can use Form 941-X to correct:

• Wages, tips, and other compensation

• Income tax withheld

• Taxable Social Security and Medicare wages and tips

• Taxable wages and tips subject to additional Medicare tax

If there is an error on a previous Form 941 that you already filed, use Form 941-X to fix the errors. You can use Form 941-X to correct both underreported and overreported taxes.

You can correct over-reported taxes on a previous Form 941 within three years from the date when you filed the incorrect Form 941, or two years from the date you paid the tax reported on Form 941, whichever is later.

If you want to apply the overpayment as a credit, file Form 941-X as soon as you discover the error and more than 90 days before the period of limitations expires. If you want to claim a refund for the overpayment, file Form 941-X any time before the period of limitations expires.

Correct underreported taxes on a previous 941 Form within three years of the date you filed the incorrect Form 941. File Form 941-X and pay the taxes by the due date for the quarter when you discovered the mistake.

The following due dates only apply to underreported taxes:

• April 30: If you discover an error in Quarter 1

• July 31: If you discover an error in Quarter 2

• October 31: If you discover an error in Quarter 3

• January 31: If you discover an error in Quarter 4

If you’re correcting both underreported and overreported taxes and are requesting a refund or abatement, file two Forms 941-X. Use one form to correct the underreported taxes and the other to correct the overreported taxes.

Ways We Look Out for Your Business From operating accounts...

Read MoreOne of the biggest problems for businesses in the world...

Read MoreAre you tired of dealing with payroll issues in the...

Read MoreWhy Was No Income Tax Taken Out of my Paycheck?...

Read MoreAre you a business owner trying to understand the complexities...

Read More